Female gamer putting her headphones on

luza studios/E+ via Getty Images

Female gamer putting her headphones on

luza studios/E+ via Getty Images

Editor’s note: Seeking Alpha is proud to welcome William Sabga-Aboud as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Corsair Gaming (CRSR), a small-cap gaming hardware company, has been on a downward spiral since its February 2021 short-lived squeeze by retail traders. However, Corsair was never a «Reddit-worthy» company to begin with. With strong growth in its topline revenues, operating margins and bottom line EBITDA during COVID-19, Corsair was a fundamentally strong company and continues to show this today. Investors have lost confidence following a global-wide chip shortage for components used in its hardware and varying freight costs outside the company’s control. But those investors are forgetting that these problems will be short-lived and that Corsair will continue gaining with the growth in the overall gaming and streaming markets. This will be achieved by focusing on its current strategy of pushing its existing gaming and components peripherals segment to market-leading positions, leveraging its brand strategy and increasing its direct-to-consumer (DTC) channels.

Corsair was experiencing modest topline revenue growth pre-COVID-19. Revenues grew roughly 17% from 937.5 million in 2018 to $1.1 billion in 2019. Much of this growth was due to higher sales of Corsair branded products and to a lesser extent the introduction of Elgato after its acquisition in 2018. Corsair has two main segments that it collects its most notable revenue from, gaming and creator peripherals (GACP) and gaming and component systems (GACS). From 2018 to 2019, 26.8% of net revenue growth came from GACP while the remaining 73.2% was the result of GACS. GACP largely consists of products like Elgato’s streaming products, headsets and SCUF related pro-controllers. Corsair’s other category contains products like high-performing microprocessors and graphics cards. Here’s the exciting part: 2020 (that dreaded year) increased Corsair’s two segments to extraordinary levels.

In 2020, net revenue grew a whopping 55% from $1.1 billion to $1.7 billion. Here, GACP grew to 31.7% of net revenues, but the segment itself gained another 245.2 million, or 83% internal growth. GACS grew to 68.3% of net revenues, but by itself grew 44.8% or 360 million. Both levels of growth were largely due to the stay-at-home orders in place, as consumers spent more time working and gaming at home as well as existing customers upgrading their gear for a better experience.

Corsair Net Revenue Breakdown

Corsair

Corsair Net Revenue Breakdown

Corsair

Other notable growth occurred in Corsair’s Gross Profit Margins and EBITDA margins.

In terms of its Gross Margins, 2019 was positively impacted by a shift in product mix but offset by a negative impact from additional tariff costs, resulting in a flat gross profit margin of 20.4%, a reduction of 0.2% from its 20.6% margin in 2018, leaving Corsair with 224.2 million in gross profit. In 2020, gross profit margins rose from 20.4% in 2019 to 27.3%, a 6.9% increase, or an increase of 241.1 million to 465.4 million in gross profit. This was largely due to increased sales volume, an improved product mix with higher-margin products and less promotional expenditures. In terms of the individual segment categories, GACP had the higher profit margin of 35.2%, while GACS held a steady 23.7% in 2020.

Corsair Gross Profit Margin

Corsair

Corsair Gross Profit Margin

Corsair

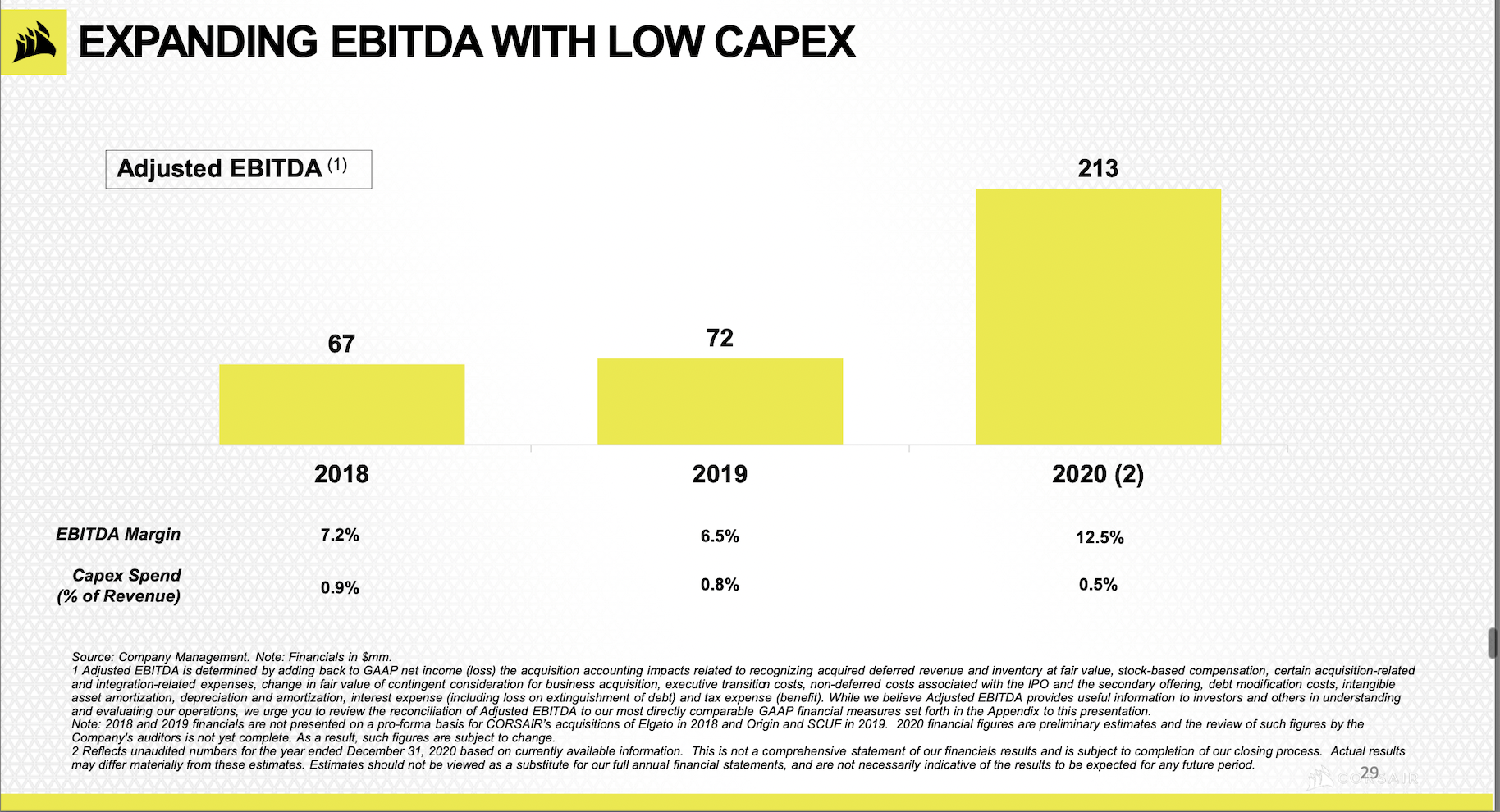

In its 2019 EBITDA Margin, Corsair fell 0.7% from 7.2% to 6.5% with a notable 0.1% decrease in CAPEX spending as a percent of revenue. However, in 2020 Corsair’s EBITDA margin rose to 12.5% with a notable 0.3% decrease in CAPEX spending as a percent of revenue. This left Corsair with adjusted EBITDA of 213 million in 2020, a 70.5% increase from the year before. CAPEX spending was 145.4 million in 2019, 126 million being the result of the SCUF acquisition. However, 2020’s CAPEX expenditure was only 10.3 million, a large reduction. This reflects Corsair’s ability to increase EBITDA while outputting less capital expenditures, reflecting its improved operational efficiencies and competitive advantages in 2020 as compared to 2019.

Corsair Historical EBITDA margin

Corsair

Corsair Historical EBITDA margin

Corsair

Overall, Corsair was a «typical» company Pre-COVID-19, succumbed by modest growth and average financial statements. However, COVID-19 propelled Corsair into hyper-accelerated growth, allowing it to sweeten its statements and position itself to capitalize on a rare opportunity to gain market share. However, we cannot see how much market share it has gained unless looking at the growth in the overall market.

In the gaming industry, there were an estimated 2.8 billion gamers worldwide spending more than $174 billion on games in 2020 alone, according to research group Newzoo. With increased variety of quality and availability, Corsair believes the gaming industry will only continue to expand. The average gaming time has increased 36% YoY and will jump from 1.1 to 1.5 hours of average gaming time in the next five years. Newzoo believes this industry will grow by a compounded annual growth rate of 8.7% by 2024. These estimates put the gaming industry’s market value to 218.7 billion in 2024.

Within the gaming industry, the PC and streaming gear market represented 36 billion in 2019. Further research reveals that there were an estimated 524 million PC gamers worldwide in 2019, of which 94 million spent at least $1000 on their gaming PCs.

In the streaming industry, there are two segments applicable to Corsair: e-sports and gaming content creation.

Corsair Predicts that the global e-sports sector will grow at a CAGR of 11.1% from 2019-2024. This is due to a growing number of gamers fueling the competitive gaming sector. In 2020 alone, there were an estimated 729 million viewers of e-sports.

In gaming content creation, there were an estimated 50 million gaming channels on YouTube and Twitch in 2021. Twitch alone has a concurrent active user base of 9.6 million creators streaming each month. In addition, there were an estimated 100 billion hours of gaming content watched on YouTube’s 40 million gaming channels in 2020. With this in mind, Corsair expects a CAGR of 13% from 2021 to 2026.

COVID-19 fueled the switch to digital and more people are becoming accustomed to desire high-quality environments for better setups to enhance their entertainment, creativity and collaboration in a digital era. A research firm called Juniper Research labeled the sector one of the fastest-growing sub-sectors in the gaming industry. They further Predict that the market value growth will be driven by subscription spending to platforms like Twitch and advertising revenues generated from such. With this, an estimated one billion people will be viewing e-sports and game-related streams by 2025.

I expect this number to grow even more. Powerhouses for streaming game content like Twitch and YouTube gaming are becoming increasingly popular. More and more people are streaming these days despite lockdowns being lifted globally. Game categories like battle royales have fueled the growth of competitive gaming and have become a pathway for competitive gamers to both earn an income and grow their influence. In addition, gaming today represents an estimated 11% of all American consumer internet and media activity, reflecting the penetration it has made into the American consumer’s way of life.

Corsair was a mixed bag in 2021. For one, Corsair resumed growth, but that growth was unable to gain anywhere near 2020 levels. On the other hand, Corsair became victim to a number of problems impacted by the global pandemic. All in all, investors’ confidence was cut and the share price has been on an epic downward spiral ever since. Let’s take a look at the year quickly and see what concerns currently exist amongst investors in order to gauge the logic.

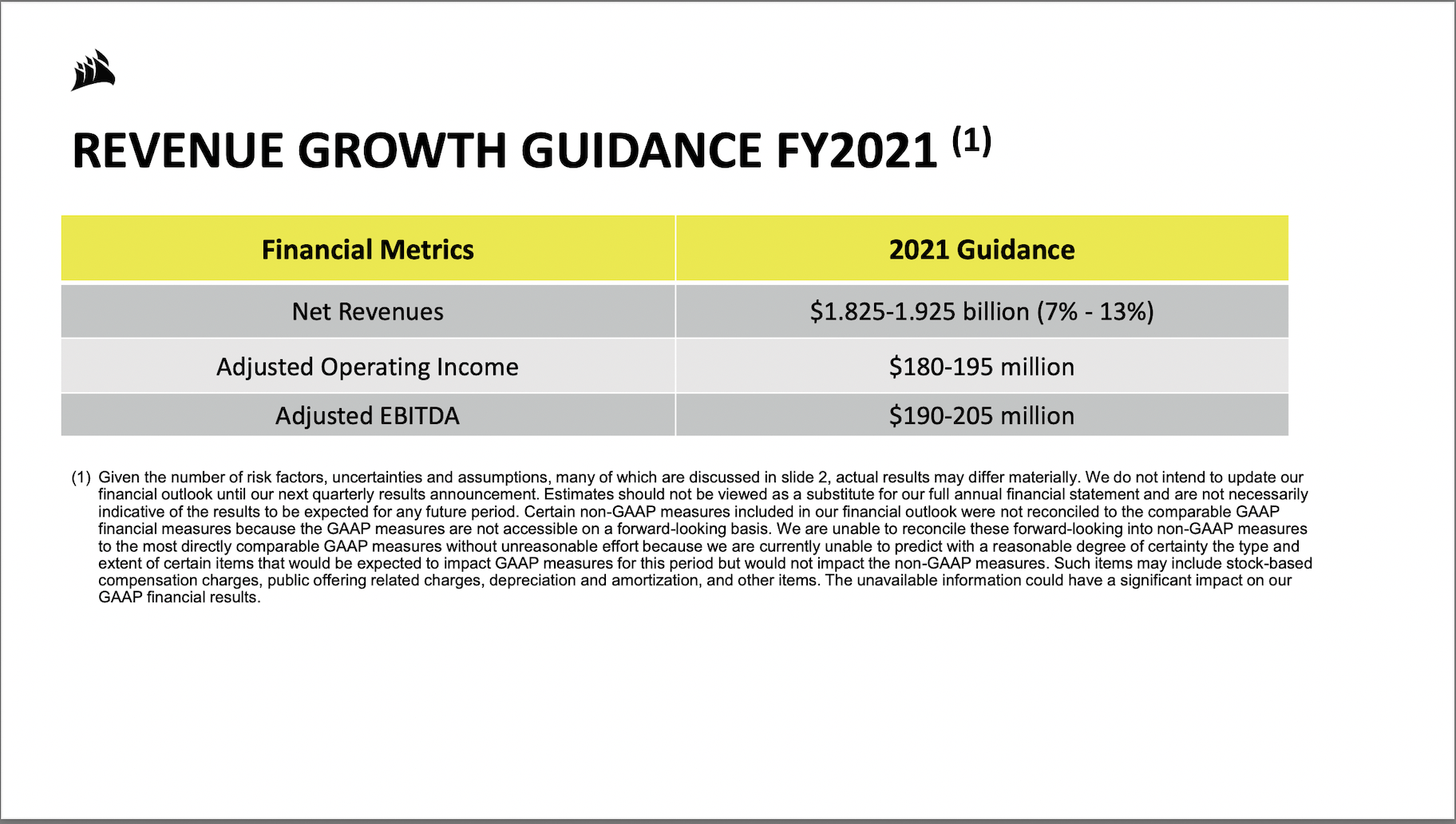

Right now, Corsair is projecting net revenues between 1.82 and 1.92 billion for the year, a pessimistic 7%-13% growth rate, far lower than its previous high of 55%. Here, net revenues were impacted by the availability of reasonably priced GPUs, curtailing the demand for new PC builds by consumers, severely impacting GACS, which holds the bulk of their net revenue. With this shortage, GPUs became scarce over the year, causing retail prices to surge to 150% of MSRP. Net revenues were impacted to a lesser extent by the shortage in IC supplies, a main component in Corsair’s high-value products.

Corsair expects adjusted EBITDA in the range of 190-205 million this year. This reflects a 3.8% decrease on the optimistic side and a 12.1% decrease on the conservative side. Much of this follows from the problems described above.

Projections by Corsair

Corsair

Projections by Corsair

Corsair

Gross profit margins are also down to 25.9%, an almost 2% decrease from its high of 27.3%. This drop was attributable to higher logistic costs and air freight.

So the year wasn’t great, but investors these days are myopic. They see one bad earnings report and ridicule the company into oblivion. This year was catastrophic. Economies were on their knees and foundations lay collapsed. However, the pandemic will end and the forces of supply and demand will rebalance the markets. With this in mind, it’s time to address those concerns.

Logic: Most lockdowns in the world have lifted in 2021. Therefore, it is reasonable to assume post gaming demand will decrease. However, the data points to the contrary opinion.

In the streaming industry, it was predicted earlier that the e-sports segment will grow by a CAGR of 11.1%. In 2019, viewership reached 729 million. With a CAGR of 11.1% YoY, there is no signs of a slowdown in growth that aligns with its exponential rise during COVID-19. In the content creation segment, Twitch has reported over 9 million active streamers on their channels and 140 million active users. That’s 40% growth from its 2015 peak of 100 million active users. Impressive to say the least, and that’s only one platform.

A picture of an e-sports event

A picture of an e-sports event

Forbes

The gaming market has an expected CAGR of 8.7% through 2024, so an already large industry continues its growth trajectory. Furthermore, gamers are «sticky.» The majority of people that play video games tend to continue playing indefinitely. It is similar to people buying an Apple product because once you do, they’ve got you; you’re locked into their ecosystem.

Andy Paul, Corsair’s CEO shares a similar opinion. He has stated that he believes there is a pent-up demand for consumers wanting to upgrade their PCs. In fact, management has expressed that current demand is equivalent to the elevated levels seen in the wake of the work-from-home situation. A report by Jon Pedie Research estimates that graphic card sales will increase from 23.6 billion in 2020 to 54 billion in 2025. Unfortunately, the global supply chain shortage of chips has caused skyrocketing price increases. Andy thinks these people will wait for prices to drop and then buy the components. His reasoning is that historically consumers upgrade their PCs every 3-4 years. However, that cycle has dropped to 1-2 years and is currently upon us.

Logic: Management has pointed out that high logistic costs continue to be problematic for Corsair. For example, ocean freight costs for 40-foot containers have increased 3-5x their normal levels. Additionally, logistics have increased, delaying some chips. It doesn’t help that most of Corsair’s products are produced in Taiwan, where it has to rely on ocean freights.

The bad news is that management estimates that these costs hurt the company’s margins by 2%-3% and are expected to continue until at least the second half of this year.

The good news is that they are doing something about it. Andy Paul has stated that what once took 6 weeks to reach the port now takes 10. However, there are more ships on the ocean. Thus, his team is planning around it. Since the balance sheet has improved, his team can simply hold more inventory to fix the supply chain. With increased demand in the market, this will likely prove beneficial in the long run.

Record backlog of cargo ships at California port

Record backlog of cargo ships at California port

BBC news

Corsair’s management has made clear that any sustained cost Pressures can be passed on to the end consumer. Andy Paul has stated that if he sees any cost that will stay for a prolonged time in the future, they will adjust that in the pricing of their products.

Now, this only means management will adjust prices on products that are unlikely to recover from the problems above. Doing so on short-term problems is problematic in a retail setting and Corsair will avoid this. The good news is that Corsair can afford to adjust its long-term problems. They don’t label themselves as a low-cost provider and instead offer Premium, quality products to consumers.

Fortunately, its competition is likely facing similar problems. Therefore, any cost adjustments by Corsair will likely be done on a similar level by Logitech or Razor. With a strong financial position, Corsair is more than capable of competing in prices. As we have seen, COVID-19 has allowed Corsair to propel into a favorable financial position, and they can experiment with the market a bit to maximize their desired margins.

All in all, both concerns will be short-lived and should not be a prominent factor for any thorough investor that invests for the long haul. That is, someone bullish on the long-term growth of the gaming and streaming markets and Corsair’s position in it.

Corsair has had a shaky two years with this pandemic. On one hand, COVID-19 has accelerated Corsair’s growth and position in a market that itself accelerated. On the other hand, it is left with a number of problems that hopefully have convinced you now are myopic in nature. While the company is doing all it can to minimize its losses from these problems, there are a number of things Corsair is currently doing well to sustain long-term growth and bounce back to the levels seen in 2020.

Corsair is already first place in every category in its GACS segment and is quickly gaining more, as shown in their Q3 report. Luckily enough, this is also the bulk of their revenue. However, we know it maintains a lower margin (23.7%) than the GACP segment (35.2%). Hardware product prices like microprocessors are sticky, and Corsair will have a hard time pushing these margins even further than their current levels in the near future. Therefore, Corsair can improve their operating margins by pushing its existing products in the GACP segment. This area is both more opportunistic and realistic for long-term sustainable growth. Corsair knows this and is constantly pushing these new channels to their max.

Over 2021, the fastest-growing categories of GACP were Elgato branded products and SCUF related items. In Q1 2021, GACP almost doubled as a result of the strong sales of these two categories. Furthermore, the segments’ gross margin increased to 39.1%, reflecting the operational efficiencies Corsair was achieving in manufacturing, marketing and selling these brands of products.

Earlier analysis revealed that Corsair is currently in second place in both streaming products and performance controllers. Therefore, there is room to grow here and is the most opportunistic route for Corsair to quickly gain market share while following its strategy of selling these products at high margins. Additionally, the streaming market has many verticals for which Corsair can produce new products and further gain ground. Last year, Corsair released 113 new products and is increasingly increasing their R&D expenditures, so this strategy will likely pan out. Lastly, pushing GCAP can take some of the Pressure off GCAS’ role of generating the majority of the company’s revenue, mitigating extraordinary factors like volatile input costs that often drive down operating margins in a dynamic product environment.

Elgato Line of Products

Elgato Line of Products

Elgato

The closest way to explain Corsair’s brand strategy is to relate it to Nike. Everyone knows Nike’s ubiquitous tick. You see it at a friend’s home, the grocery or a movie theater. The tick is imbedded in everyone, whether or not they consume the products. Nike’s success with its branding strategy is a direct result of this. However, much of this is fueled by contract deals it signs with super-athletes to represent the brand. Both Cristiano Ronaldo and Lebron James have billion-dollar deals with the shoe company, requiring that they wear the brand in games or in public. This has proved quite successful, or Nike wouldn’t be signing billion-dollar deals.

Corsair’s simple logo boasts a simultaneous display of simplicity and quality. The black sails followed by the name in a yellow backdrop are recognizable and memorable. It is also ubiquitous, just for a different kind of market. You see, where Nike is outdoors, Corsair is indoors, or better yet, digital. Turn on your computer and head over to Twitch or YouTube gaming and look at the logo on the side of the gamer’s head. If it’s not Corsair, I’d be surprised. That’s because Corsair has signed over 800 professional and nonprofessional gamers over the years. This boasts a reach of over 1.3 billion people.

One sponsorship of recent importance is the gaming group, BIG. Corsair recently extended their contract with the e-sports giant for another two years in May of 2021. Daniel Finkler, the CEO of BIG has stated, «We value loyalty and trust very highly. And Corsair has been by our side through all our phases, in good times and bad. Corsair’s gaming peripherals are high quality, precise, and best suited for ambitious gamers, and we are proud to represent such a renowned brand with our athletes around the globe.»

Additionally, Corsair is promoting a diverse set of sponsorships, evident by its recent partnership with T-Pain branded headphones. This shows Corsair’s outside-the-box attitude to not only partner with e-sports contenders but other areas of interest. Corsair has shown that they understand their demographic, and that by selling to both e-sports professionals and gaming fans, they have the potential to be as ubiquitous as Nike.

Corsair brand

Corsair brand

Amazon

The brand’s social media presence has also been growing, contributing to the Nike-esque strategy of the digital world. Head on over to their Instagram account and you will see over 2.8 million followers on their main channel and another 4 million on their affiliates. By contrast, their biggest competitor, Logitech only has 712,000 followers on their main channel. Corsair’s Twitter reach is around 6.8 million and Facebook another 4.2 million. Nonetheless, this further reinforces the fact that Corsair is reaching its audience across the digital world, not the physical. Yes, you get a physical product, but its marketing and presence are only really Present digitally, separating them from brands in both their own industry and outside of it.

If this trend continues successfully, Corsair will have leveraged the brand against the growth in the overall market and see a plethora of new users. In the end, Corsair will have its topline revenues to thank for the newfound growth. Something I think this current strategy will prove undoubtedly successful.

Corsair social media presence

Corsair

Corsair social media presence

Corsair

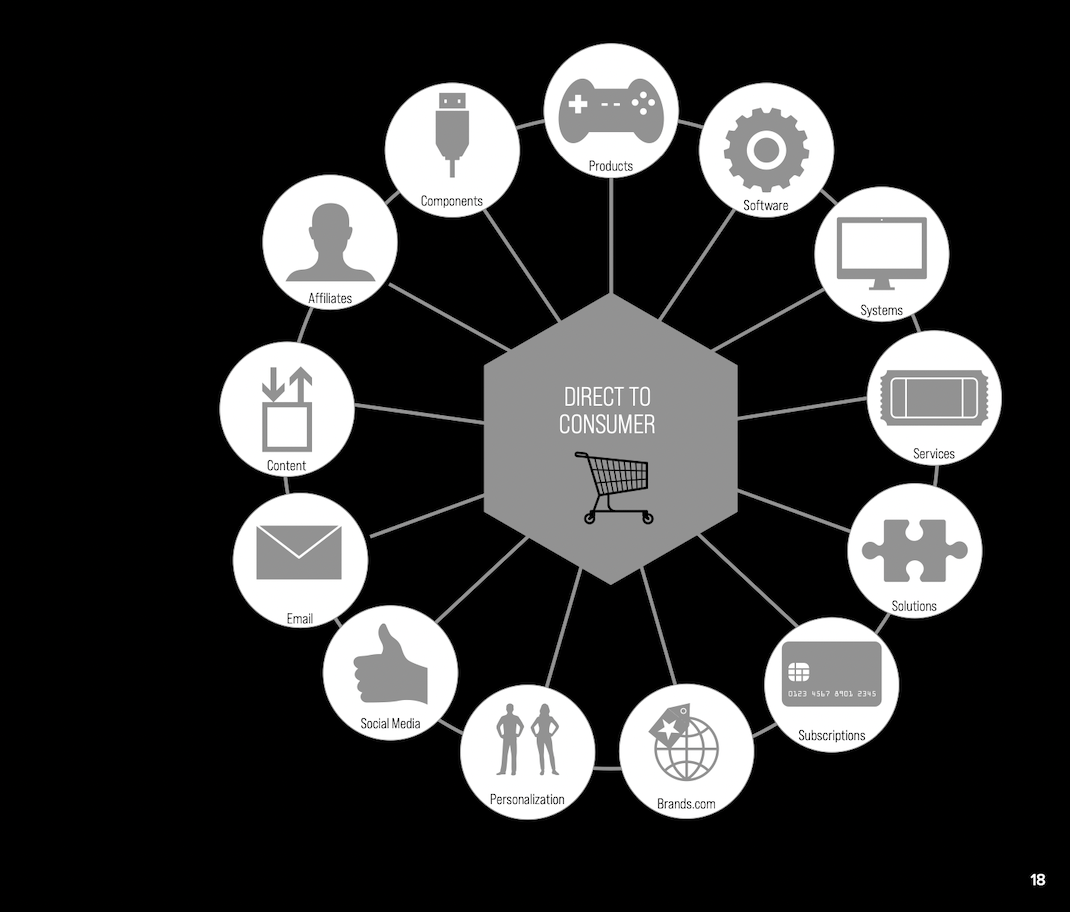

In 2020, 20% of Corsair’s overall sales came from Amazon.com. The problem with selling on a third-party platform is that the company has little say in its pricing prospects. They will sell on Amazon, which gets a percentage for each product sold, cutting into their gross profit margin. Corsair knows this and has been pushing its direct-to-consumer sales channels more frequently.

Corsair plans to have 15% of revenues coming from DTC channels by 2023. Much of its affiliates like Elgato and SCUF were already generating revenue through its DTC channels. For instance, in Q3 2021, DTC sales were 13.1% of net revenue, up from 10% a year earlier. These brands are also some of their most profitable enterprises. Therefore, there is much value to be added from increasing existing channels and introducing new ones. Let’s assume for a second that Corsair does achieve 15% of net revenues coming from DTC. Let’s also very conservatively assume Corsair achieves 1.9 billion in revenue this year and grows at only its most conservative rate projected for the next year, 7%. By the beginning of 2023, Corsair would have approximately 2.1 billion in net revenue. If 15% of revenues are DTC, then roughly 315 million dollars will be applicable to the better DTC margins, greatly improving EBITDA and net income.

Corsair DTC strategy

Corsair DTC strategy

Corsair

I expect revenues as a percent of DTC channels to grow as the company improves the efficiency of these channels and creates new ones. They have already achieved this with the channels provided by their affiliates but will continue this trajectory with the investments it has made into the infrastructure, technology and domain to support multiple consumer touchpoints. One of which is their website, which boasts a great UI (user interface) and great marketing towards their products. I am confident in Corsair’s ability to achieve long-term growth in pivoting away from third-party sellers and moving to their own channels, a sure-fire way to increase EBITDA and increase engagement with their customers.

Corsair had a rocky ride these past few years. What began as average growth and financial stability turned into an unimaginable projection of hyper-accelerated growth during COVID-19.

Ironically, COVID-19 helped both Corsair and the overall gaming and streaming markets gain a quick jumpstart. Though the growth was short-lived, I believe Corsair is addressing investors’ current concerns both strategically and effectively. Furthermore, the company is following a powerful growth strategy of increasing its GACP channels, leveraging its brand strategy to the digital world and increasing its DTC channels.

Investors are myopic, and unfortunately do not see this. Instead, they wait for the current problems to show a silver lining as reflected in the share price. However, that silver lining was there pre-COVID-19 and will be there after it. Therefore, I am rating Corsair a strong buy for long-horizon investors.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of CRSR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

de Juego de Tronos(Game of Thrones)")

{kind=link}