Sezeryadigar/iStock via Getty Images

Sezeryadigar/iStock via Getty Images

Skillz Inc. (NYSE:SKLZ) presents a unique proposition of gaming ( including games development ) while earning cash at the same time, placing the company within an interesting grey zone. In 2021, SKLZ has also been expanding its portfolio by acquiring Aarki, a leading AI-enabled advertising and marketing platform, and investment in Exit Games, a company offering Multiplayer Racing, Shooting, and Fighting Games.

However, with a less than satisfactory report card for FQ4’21 and the recent market correction surrounding tech stocks, the market sentiment has obviously been lagging, triggering massive sell-offs and a decline in SKLZ valuations. Nonetheless, we expect a quick turnaround for FY2022, given its reduced spending on marketing expenses and enormous potential through cloud gaming and collaboration with the NFL.

The global gaming market is also expected to grow from $203.12B in 2020 to $545.98B in 2028, at a CAGR of 13.2%. In addition, Goldman Sachs Group Inc. projected that the online sports gambling market in the US will grow from $1B in 2021 to $8.5B in 2028, at a CAGR of 35.7%. Given how SKLZ actually blurs the boundaries between gaming and gambling, we expect the company to do well indeed, despite the cultural stigma attached to it.

In its recent Investor Day presentation, SKLZ CEO Andrew Paradise revealed the company is developing a cloud-based gaming platform that would be embedded in a playable advert. When a player taps on an ad for the SKLZ game, they will be taken directly to the game, instead of being directed to the app store. The strategy would help it reach new Android users and increase the visibility and penetration rate of the company’s games to new players.

Google

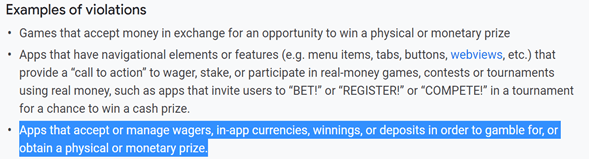

However, in our opinion, the reason for the cloud strategy is more linked to Alphabet’s (GOOG) company policy of not allowing «real-money gaming apps.» Based on its policy, «apps that accept or manage wagers, in-app currencies, winnings, or deposits in order to gamble for, or obtain a physical or monetary prize» are considered as violations. Obviously, this is aimed at SKLZ.

By adopting cloud technology, SKLZ would eventually sidestep the Google Play Store, which currently does not accept many games developed with the company’s tools. It would allow the company to reach more Android smartphone users, who accounted for over 70.97% of all smartphones used globally. This will bring the Total Addressable Market for SKLZ to over 4.71B of untapped gamers. As a result, SKLZ’s decision to go with the cloud technology is definitely not by accident, given the massive revenues and user acquisition we can expect moving forward.

The NFL-themed mobile games are also expected to be launched in September 2022, ahead of the NFL season. NFL and SKLZ have also pledged marketing support for the new games, potentially increasing its Monthly Active Users (MAU) and paid user conversion rate moving forward. In addition, a multi-year partnership between SKLZ and NFL could generate recurring revenues and convert many fans into long-term SKLZ users. With a soft launch expected from 23 March 2022 onwards at the 36th Annual Game Developers Conference, we may expect improved valuations for SKLZ, assuming widespread adoption and engagement.

Given SKLZ’s «100-year vision for building the competition layer for the internet,» it is evident that its ambition lies beyond the gaming industry. We have seen the company expand to include sports through its NFL collaboration, casual e-sports wagering, and some form of online casino. In addition, by leveraging the Metaverse concept, we expect SKLZ to easily add another layer of competitive betting into future AR/VR-enabled games in the future.

In the next decade, we also cannot rule out the possibility of group games similar to Call of Duty or Fortnite, where the monetization rate could be much higher and more profitable for SKLZ. Though highly speculative, we also acknowledge that it would require massive capital that the company currently does not have. Moreover, SKLZ’s competitors are also free to use similar strategies to monetize their games. As a result, the gaming realm will likely remain highly competitive, given many deep-pocketed game developers. Nonetheless, we expect SKLZ to capitalize on the growing mobile gaming and report robust growth moving forward, assuming successful execution and strategic capital allocation.

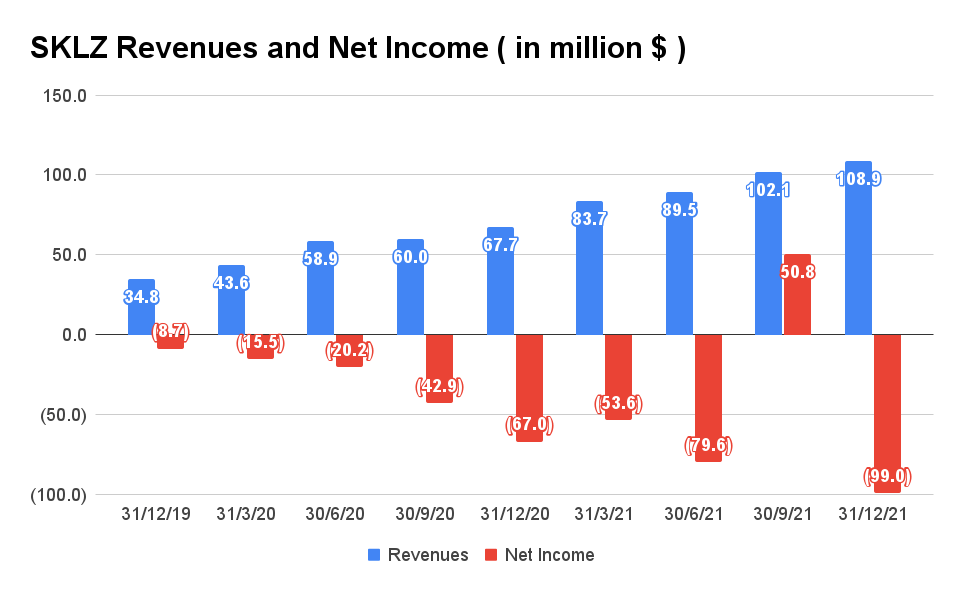

SKLZ Revenue and Net Income

S&P Capital IQ

S&P Capital IQ

Over the past three years, SKLZ reported massive revenue growth at an impressive CAGR of 96.3%. In FY2021, the company reported revenues of $384.09M, representing remarkable YoY growth of 66.9%. For FQ4’21, SKLZ also reported record-breaking revenues of $108.9M, representing exceptional growth of 6.6% QoQ and 60.8% YoY. In addition, it is worth mentioning that the company boasts impressive gross margins at 93.6% for FY2021. SKLZ also reported excellent growth for Paying Monthly Active Users (PMAU) at 56% YoY to 0.61M, with Average Revenue Per Paying User (ARPPU) increasing 3% YoY to $59.

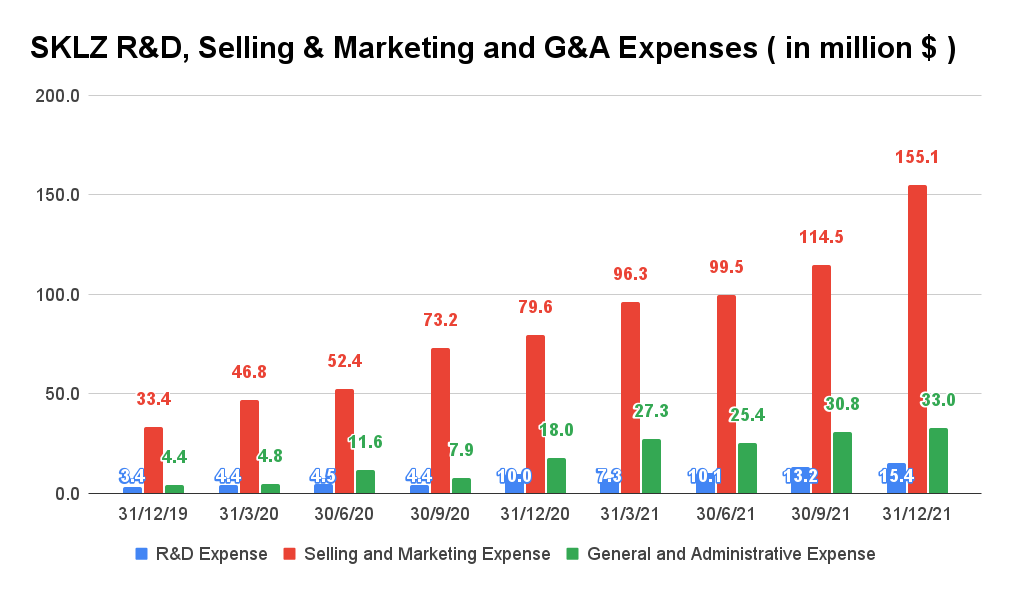

SKLZ R&D, Selling & Marketing, and G&A Expenses

S&P Capital IQ

S&P Capital IQ

However, SKLZ’s net losses widened to -$99M in FQ4’21, given its aggressive expenditure for marketing purposes at $155.1M. The fact that the expenses were not reflected in the profits alarmed investors and prompted a massive sell-off triple the usual trading volume. Consensus estimates that SKLZ’s growth may finally be slowing down, post COVID-19 pandemic. Nonetheless, with the company pledging moderation for its engagement marketing and user acquisition budgets, we expect improvement in its operating and net income from FQ1’22 onwards, as iterated during the FQ4’21 earnings call on 23 February 2022.

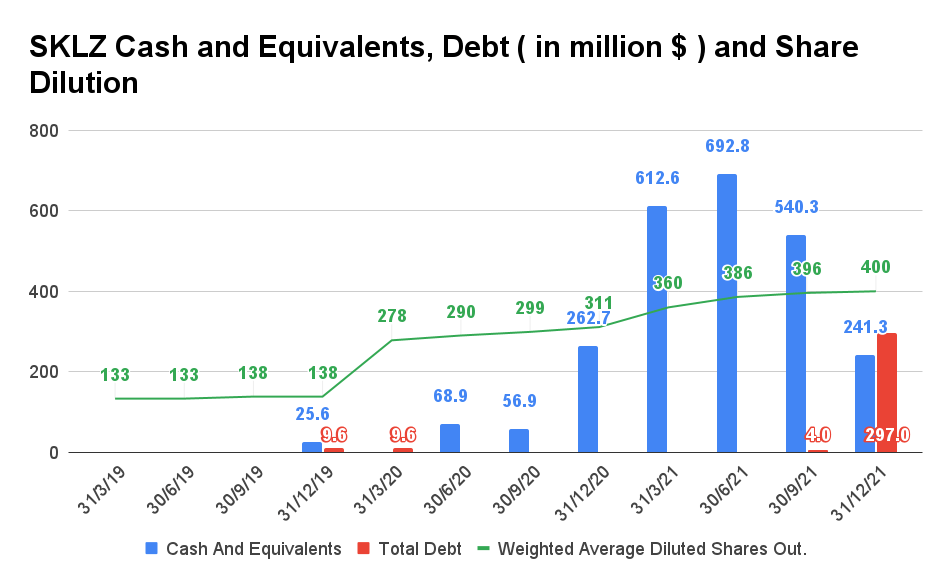

SKLZ Cash and Equivalents, Debt, and Share Dilution

S&P Capital IQ

S&P Capital IQ

Nonetheless, since the company has yet to report profitability, SKLZ has been relying on a combination of debt and share dilution to fund its operations. As of FQ4’21, SKLZ has 399M shares outstanding, representing 28% dilution YoY. In addition, the company raised $300M of debt due 2026 at 10.25% interest in December 2021.

It is evident that SKLZ has used up all of its cash from the IPO in December 2020, given its cash and equivalents of $241.33M as of FQ4’21. As a result, since the company will not be reporting profitability in the next few years, SKLZ may continue to rely on similar strategies to raise funds.

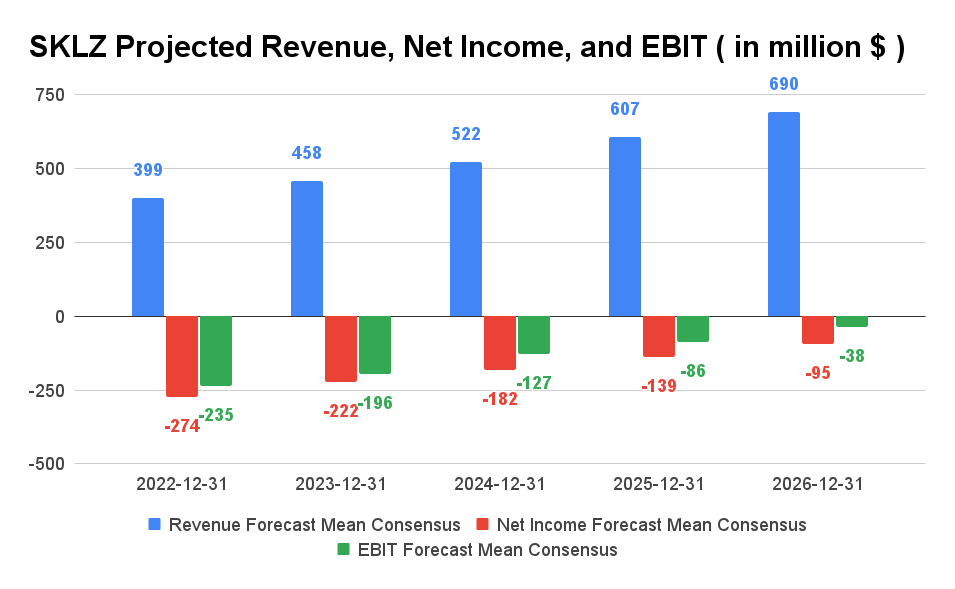

SKLZ Projected Revenue, Net Income, and EBIT

S&P Capital IQ

S&P Capital IQ

SKLZ is expected to report an apparent deceleration of revenue growth at a CAGR of 12.44% over the next four years. The historical revenue growth was obviously unsustainable, given how the company guided revenues of $400M for FY2022, in line with FY2021 revenues. The lower revenue guidance than consensus’ previous estimates of $548.78M and deceleration of growth has also hurt its stock valuations, given how it fell -11% post FQ4’21 earnings call. In addition, with ongoing marketing, R&D, SG&A expenses, and slowing revenue growth, consensus estimates SKLZ will not be net income and EBIT profitable in the next four years.

Nonetheless, post the F4’21 earnings call, SKLZ still retained its guidance to report EBITDA breakeven by FY2024. In addition, we must also note that its $400M revenue guidance for FY2022 does not include the upside contribution from the NFL collaboration. As a result, we expect an upward rerating of approximately 10% or even more for the fiscal year, with FQ1’22 earnings expected to exceed consensus estimates due to its better grasp on marketing expenses.

We surmise that the revenue growth experienced during the COVID-19 pandemic was simply a pull-forward effect from the lockdown period in the past two years. SKLZ is currently trading at an EV/NTM Revenue of 2.11x, lower than its historical mean of 13.92x. Given the market correction surrounding high-growth stocks, SKLZ stock is also trading at bottom prices of $3.14 ( as of 21 March 2022 ). As a result of the moderation, we believe SKLZ is currently trading nearer to its normalized valuations.

We also would like to highlight that almost all gambling stocks out there are being punished, with DraftKings (DKNG) and Penn National Gaming (PENN) losing -64.39% and -38.26% of their values in the past six months, respectively. Even gaming companies such as Take-Two Interactive Software (TTWO), Sea Limited (SE), and Roblox (RBLX) have declined by -21%, -65.32%, and -40.88% within the same period, respectively. As a result, we believe SKLZ’s 90% discount from February 2021’s highs of $43.72 looks appealing for investors seeking bargain prices for speculative gaming stocks.

Of course, those who have bought at the higher prices would have experienced maximum losses. We would like to extend our regrets, since SKLZ is not expected to reach those levels soon.

Therefore, we rate SKLZ stock as a Buy only for long-term speculative investors.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

de Juego de Tronos(Game of Thrones)")

{kind=link}